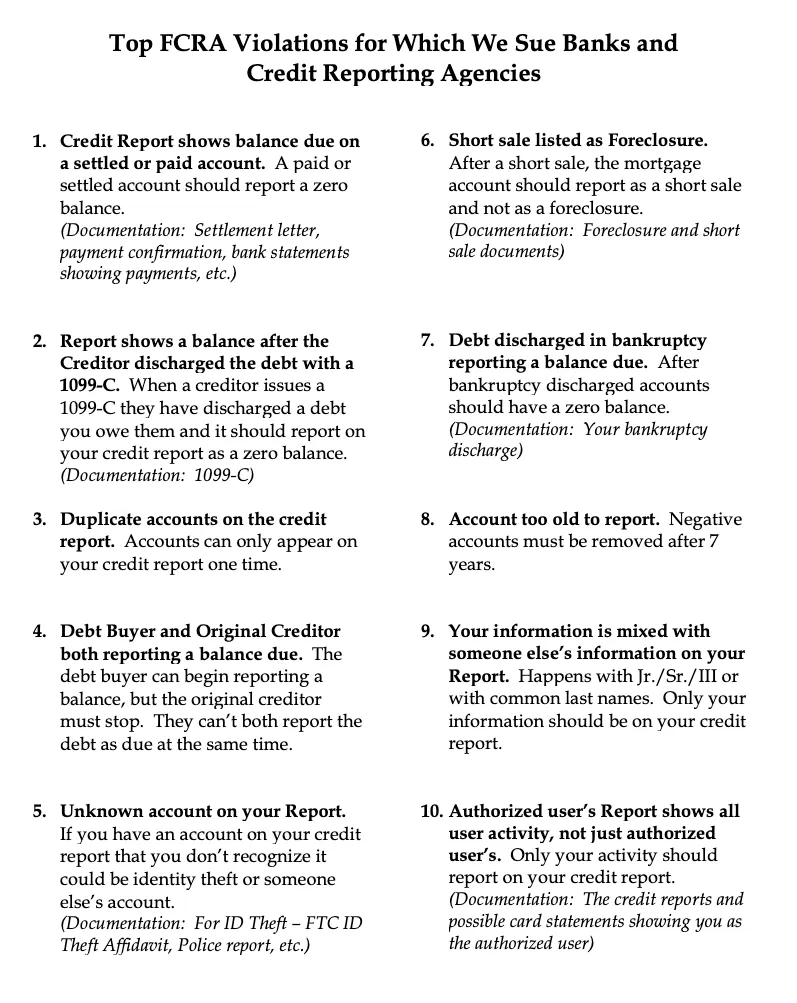

Key IRS Rules for 1099-C Issuance

The IRS requires creditors to file Form 1099-C (Cancellation of Debt) only when:

- The canceled/forgiven debt is $600 or more (principal amount).

- An “identifiable event” occurs that signals the debt is officially canceled (not just charged off).

- The creditor is an “applicable entity” (banks, credit card companies, etc.).

A charge-off itself is not an identifiable event — it’s an accounting write-off where the creditor stops expecting full payment but may still pursue collection (sell to debt buyers, etc.). So many charge-offs never trigger a 1099-C.

Common “identifiable events” that do trigger a 1099-C include:

- Creditor’s internal policy to stop collection and discharge the debt (most common for credit cards).

- Expiration of statute of limitations for collection.

- Settlement for less than full amount (e.g., you negotiate payoff for 30–50%).

- Bankruptcy discharge.

- Creditor decides debt is uncollectible (sometimes after years of no payments).

How Often / Likelihood After Charge-Off

- Not very often immediately — Charge-offs happen ~180 days after last payment, but creditors often wait 1–3+ years (or never) to officially cancel and issue 1099-C.

- Likelihood: Roughly 30–60% of large credit card charge-offs eventually get a 1099-C (based on tax professional forums, debt relief reports, and IRS data trends). Many debts are sold to collectors instead of canceled outright.

- Timeline if they do issue one:

- Creditor must send by January 31 of the year following the cancellation year.

- Example: Debt canceled in 2025 → 1099-C by Jan 31, 2026.

- Some wait 1–4 years after charge-off (e.g., after selling debt or statute expires).

- Never issued: If debt is sold/transferred, collector may continue collection without canceling, so no 1099-C.

Bottom Line

- A charge-off alone does not mean you’ll get a 1099-C or owe taxes on it.

- You only report canceled debt as income if you receive a 1099-C (or know debt was forgiven >$600).

- If you get one years later → it’s still valid (creditor can issue anytime they cancel).

- If no 1099-C → no tax reporting needed (even if charged off).

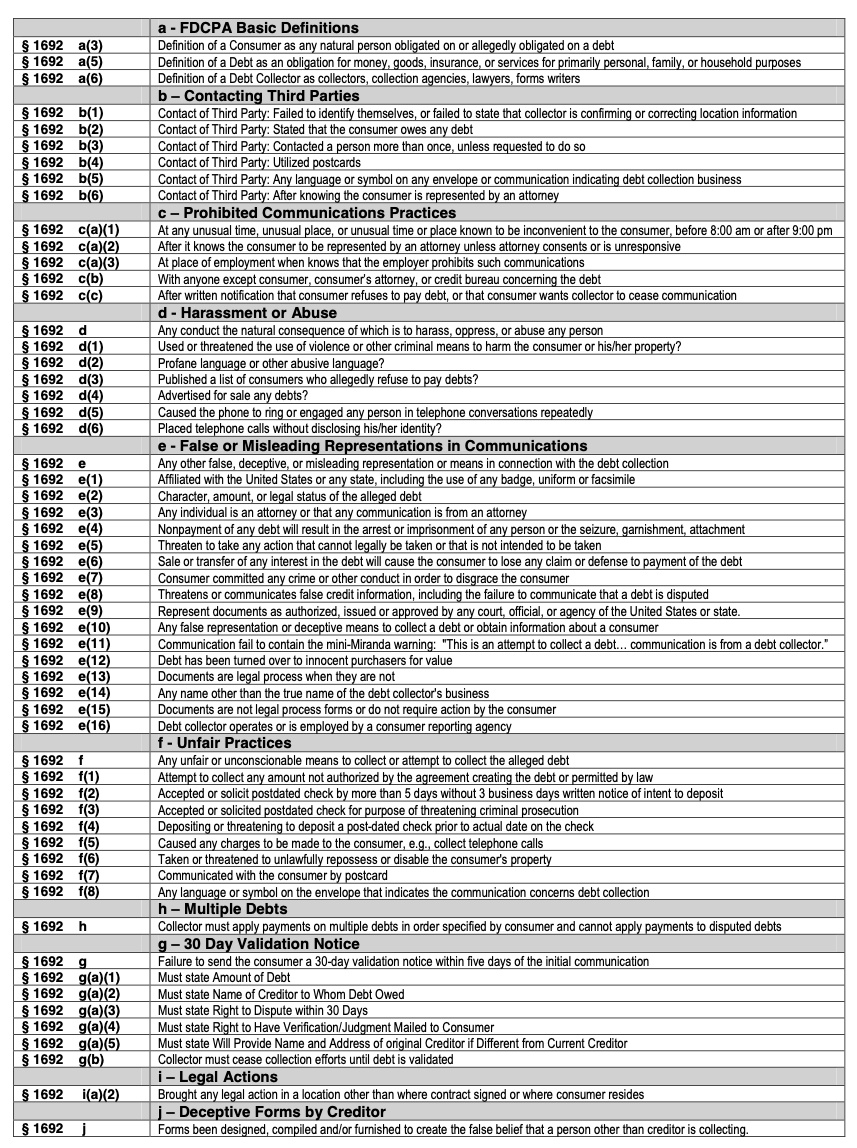

Top FDCPA Violations

Know Your Rights

Or Debt Collectors Win

Debt collection agencies rake in money. Big money. It’s a $13 billion industry. But those numbers – as staggering as they are – tell only one side of the story. The other side is the story of the 77 million Americans who have debts in collection.

One in three Americans has a bill that has been sent to a debt collector. The average debt in collection amounts to $5,178. Last year, debt collection agencies collected $55 billion, and raked in more than $13 billion in profits. A third of that came from debt buyers, who purchased charged-off debt for pennies on the dollar.

Most Americans don’t know their rights. Every day, debt collectors coerce, intimidate, threaten, and harass consumers into paying money they may or may not owe. When they use those tactics, debt collection agencies are in violation of the Fair Debt Collection Practices Act (FDCPA).

The FDCPA makes a number of debt collection tactics illegal, including:

- Calling multiple times per week

- Calling before 8:00 a.m. or after 9:00 p.m.

- Calling your workplace

- Using profane or abusive language

- Threatening to sue you, harm you, or destroy your credit

- Talking to others about your debt

- Calling repeatedly for the wrong person

- Failing to notify you of your right to dispute the debt

- Failing to send you a letter within five days of their first phone call

- Telling you that you’ve committed a crime

- Contacting you after you’ve asked them not to

- Threatening to take legal action on a debt that’s past the statute of limitations

There’s another law that debt collection agencies (and creditors) are known to violate: the Telephone Consumer Protection Act (TCPA). When a debt collector or creditor robocalls your cell phone using an automated dialer or a pre-recorded voice, they’re likely violating your rights.

The FDCPA and TCPA don’t just protect those who owe money; the law protects anyone who is contacted by a debt collector. So, for example, if you keep getting hounded by a debt collector who’s calling for someone you don’t know, that’s against the law. The same holds true if a collector keeps calling you to talk to a relative who doesn’t live with you. Or if a creditor robocalls your cell phone multiple times.

Knowledge is power. When you understand what debt collectors and creditors can and cannot do under the FDCPA and TCPA, you can make them pay you.

Under the law, you can sue in federal court and recover up to $1,000 for debt collection abuse, and up to $1,500 per call for cell phone robocalls.

When you’re ready to fight back, you need an attorney by your side who has deep knowledge of the FDCPA and TCPA, and who has vast experience in holding debt collection agencies and creditors accountable. That’s where Lemberg Law comes in. Every day, we go toe-to-toe with the bad players in the debt collection industry. You can count on us to stand up for your rights and deliver the justice you deserve.

You have rights. We’ll enforce them.

FDCPA Texas Cheat Sheet